There is a movement happening across a range of sectors that we need to be aware of.

Across multiple regulators, there is an increasing focus on consumer understanding, and preventing harm and confusion by ensuring that key disclosures are made more intelligible.

The Consumer Rights Act is the fundamental pillar of consumer protection in the UK. It has always included the need for consumer terms to be intelligible - i.e., able to be understood, and the information applied by consumers. Yet only recently has this come under real focus.

The Digital Markets, Competition and Consumers Act (DMCCA) last year gave the Competitions and Markets Authority (CMA) sweeping new powers to directly enforce the Consumer Right Act. Their fining powers are now enhanced, with up to 10% of a firm’s global turnover a possible penalty.

As a result, the focus on transparency and understanding is widening across many consumer sectors. The CMA’s new Draft Guidance on Unfair Terms has been rewritten to make expectations and standards much clearer. Transparency and fairness are fundamental legal concepts, and are the basis for consumer protection and ultimately what makes a contract enforceable. Both concepts are underpinned by intelligibility.

The new CMA guidance is expressive of the need for well-structured and navigable information, that sets out the key information clearly and able to be understood by even unsophisticated consumers.

The recent Motor Finance legal case and a compensation bill of upwards of £8 billion has also focused the minds of risk and compliance professionals. The legal challenge was eminently avoidable by the industry, yet technical disclosure was again placed before achieving positive outcomes for the consumer.

But this changing.

A move towards better outcomes

At present, the form and format of disclosures prescribed by law and regulation continue to be the dominant influence on how firms communicate, from pre-sales information, terms and conditions, contractual agreements, to post-sales communications. These rigid disclosure rules often work at odds with the ability of consumers to understand the communications. This misalignment of regulatory objectives enables some firms to justify or excuse why their terms are still unnecessarily complex.

In financial services, the Consumer Duty has already shone a harsh spotlight on the need for firms to change tack. And other sectors are now following suit.

Part of the problem is that to simplify their disclosures, firms are still relying on readability models such as Flesch Kincaid (which, while sounding very complex, is solely based on sentence length and the average number of syllables). The many tools based on readability only address one part of what makes communications intelligible. In reality, this simply does not meet legal and regulatory requirements. On their own, great readability scores can create compliance risks for firms, and a false sense of confidence, never mind the risk of poor outcomes for consumers.

Using readability-based tools are driving compliance reports that are founded on entirely the wrong measure.

The move to remove prescription and shift to a focus on better outcomes is driving change. But, even under existing rules, there is still a lot more that firms can do to mitigate their exposure to intelligibility risk and improve understanding for consumers.

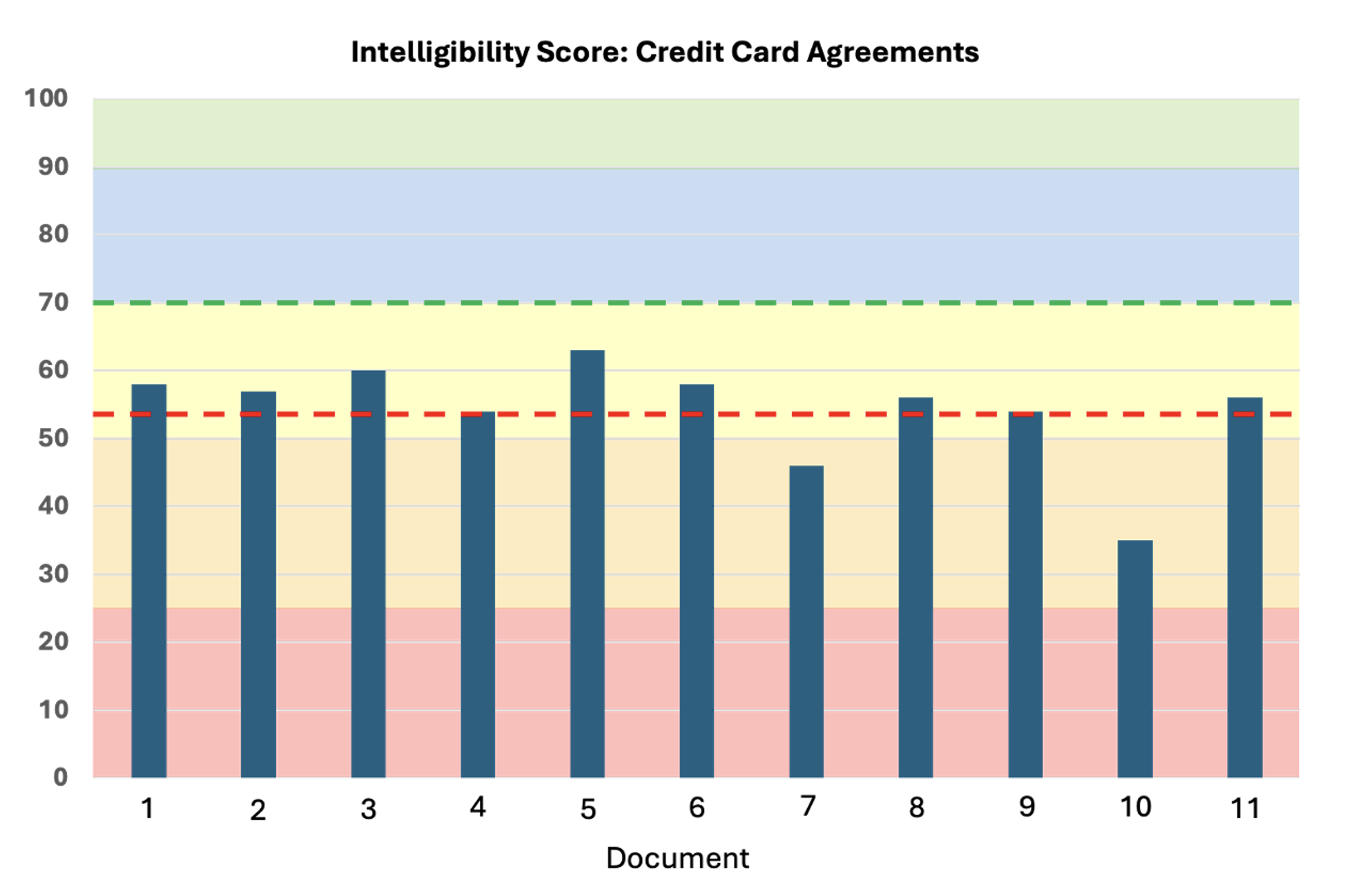

In the image below, credit card terms and conditions (downloaded from company websites in 2025) were assessed using the Amplifi Intelligibility Assessment method. It’s a science-backed approach developed with direct FCA support and already used by regulators across a number of sectors.

The assessment showed just how much they vary in how intelligible they are. This is despite them containing a very similar range and depth of information, and almost identical product features.

None of the agreements we tested met what we would consider as being a satisfactory level of intelligibility. The Amplifi Intelligibility Score ranges from 0-100, from least to most intelligible, and a common benchmark for most communications we test is 70+, represented by the green dotted line in the chart above.

However, the results varied widely. The best we tested scored in the high 60s, falling within the yellow band in the image. These are capable of being fully understood by around 70% of the adult UK population, and equivalent to a high A-Level grade paper.

The worst scored below 40. We would consider this to be in a high-risk category, and a conceptually challenging read for most people. They would be fully understood by only around 30% of adults, and equivalent to an undergraduate level paper in terms of their complexity.

Despite the legal requirement for intelligibility, significant complexity was present and wasn’t explained in simpler, more understandable terms. The documents are structurally dense, and full of technical and legal terminology. This creates a major problem for many readers.

Without addressing these challenges for consumers, and embracing better ways to test and address intelligibility, boards and senior management are simply unaware of the compliance risks they face.

Outside of financial services, the situation is equally concerning. Without the impact of the Consumer Duty’s focus on understanding outcomes, many consumer-facing communications are even more complex.

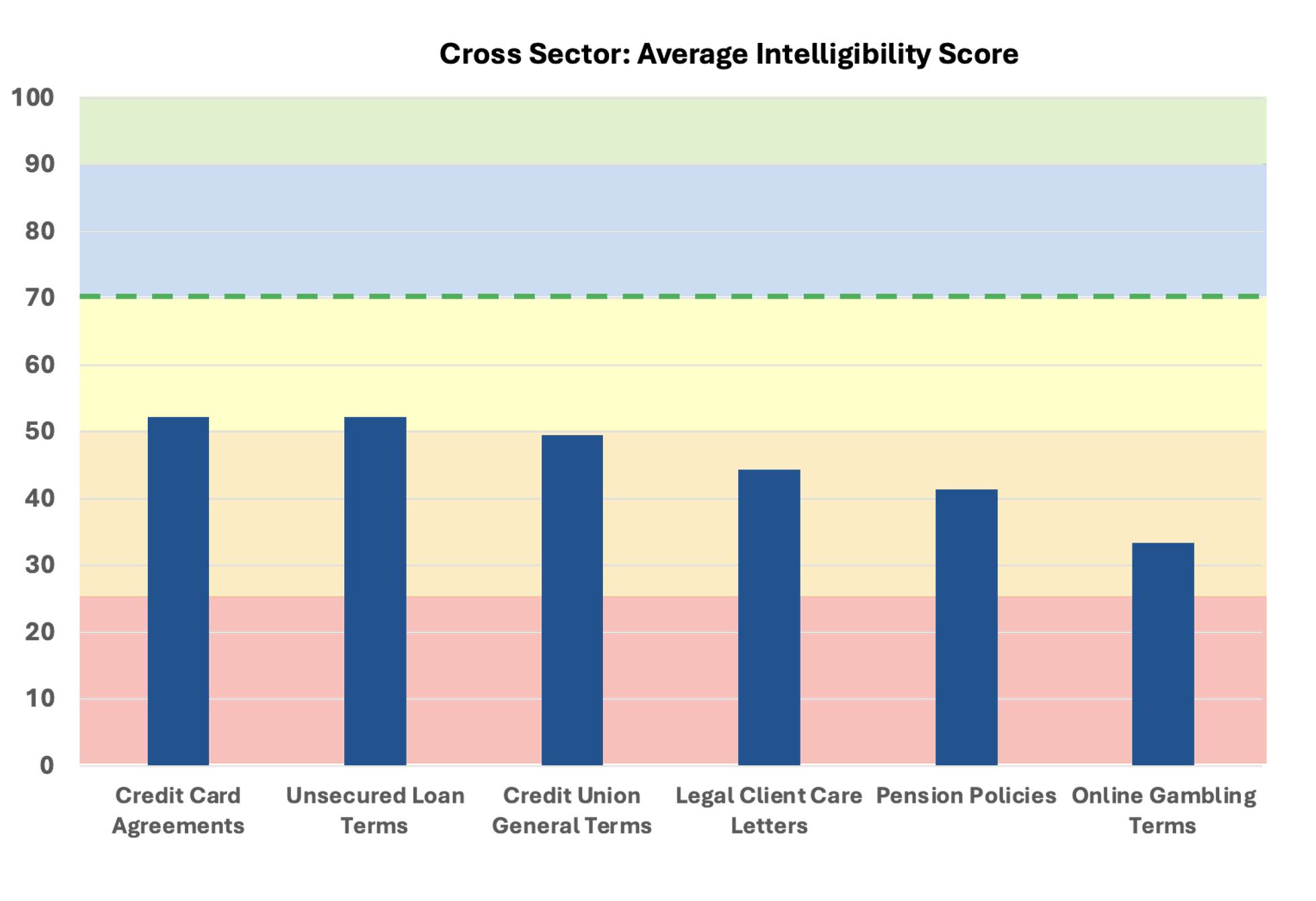

The diagram below expands the focus, to compare the average intelligibility score of key documents across multiple sectors.

Most fall short of the benchmark of achieving an Amplifi score of 70 – this is what most of our clients set for their compliance checks. Gambling terms are particularly challenging.

Gambling operators ought to be concerned, especially given the Gambling Commission has recently adopted the DMCCA into their rules and the industry’s Licence Conditions and Code of Practice. The Act gives the CMA direct oversight powers; they can enforce breaches of the Consumer Rights Act (where the need for intelligibility and transparency originates) directly, without reverting to court, and can apply their significant fining powers.

If terms are not transparent they may be unenforceable, and lead to a legal challenge similar to the motor finance case. We’ve shared our evidence with the Commission and firms, and hope to see revisions shortly.

Supporting data-driven compliance

At Amplifi we recognise the need for high quality data and a clear audit trail. Regulators, including the FCA, increasingly require firms to provide outcome evidence and rich data to support their regulatory compliance. Firms must track, and report, how they are managing their regulatory obligations.

We see firms beginning to embrace this in their everyday compliance and risk operations. And where financial services lead, many more will typically follow.

Clarity of contracts and key documents is a big area of focus. But unless the communications from firms and the outcomes for customers are properly tested, using reliable methods and with a clear audit trail, the risk for firms and consumers will continue.

Better to rip off the plaster of ignorance that currently hides the risk. Instead, embrace better data, clearer communications, and a better outcome for all.

This blog was written for The Risk Coalition by Ewan Willars. Ewan is Regulatory Lead for Amplified Global, whose intelligibility assessment technology is used for testing and compliance by firms and regulators across multiple sectors. He is a policy professional, formerly a Director for Retail Banking at UK Finance and a consultant. If you’d like to know more about hidden intelligibility risk, how to uncover it or improve your communications, you can contact Ewan at ewan@amplified.global.