In recent years, audit failures have raised concerns about the effectiveness of the auditing profession and its ability to identify and address potential risks. Why do audit failures happen, and how can they be prevented? A new approach, based on big-data mining combined with powerful analytics, provides the basis for a risk-based approach that could enhance effectively Audit quality and restore confidence in auditing.

The challenge

Having served on the Audit and Assurance Council of the Financial Reporting Council, I witnessed first-hand several audit failures that afflicted the industry, with a significant financial and reputational cost to the audit firms. Human errors, complacency, and misleading clients indeed played a role, but it was the misallocation of scarce resources together with time pressures that were also the main culprits.

Precious time is wasted by auditors who check inconsequential areas and insufficiently scrutinise areas of concern. Auditors are tasked with examining hundreds of companies with limited time, staff and budget. It's a daunting task, to say the least. They thus need a way to quickly determine which companies require extra attention and which ones might be brewing trouble.

Harnessing big data and a risk-based approach

For Audit, a solution using big data requires a stringent focus on data integrity and data quality. This is a pre-requisite to avoid “garbage in, garbage out” and ensure the quality of the output, a must for auditors. Then, a systematic approach to large-scale data processing needs to be implemented to make sense of the data and ideally produce like-for-like comparability between companies with fundamentally similar characteristics.

This transformation process brings clarity to complexity and allows for benchmarking. The ability to benchmark then empowers auditors to comprehensively understand each entity and its environment, and to focus their efforts on companies exhibiting anomalous performance relative to the benchmark, thereby allocating resources more efficiently.

The power of early indicators

The case of Patisserie Holdings plc (also commonly known as Patisserie Valerie), a UK-based café chain that collapsed due to fraud, is a good illustration. In retrospect, the company's reported figures appeared to present a picture of a well-managed enterprise on a steady growth trajectory. However, by examining the financial performance relative to its peer group, worrying disparities emerged, several years prior to its final demise.

Patisserie Holdings stands out distinctly from its peers when visualising their financial performance with the lens of a big-data solution (as Illustration 1 indicates). This could have raised suspicions and have prompted auditors to subject the company to further scrutiny. Using this benchmarking approach, auditors could have identified specific areas in the income statement that statistically deviated significantly from the peer group's average. This might have enabled them to ask the right questions and investigate areas of potential concern more thoroughly.

Illustration 1: In the graph above, each point is a multi-dimensional measure of financial performance (including EBITDA margin) and represents an entity's reported financial year. Here, Patisserie Holdings plc's financial performance stood out inexplicably (in the red box) compared to the cluster of peers for the whole period prior to bankruptcy. (Source: Lavenham Solutions - AuditBIS)

Delving deeper

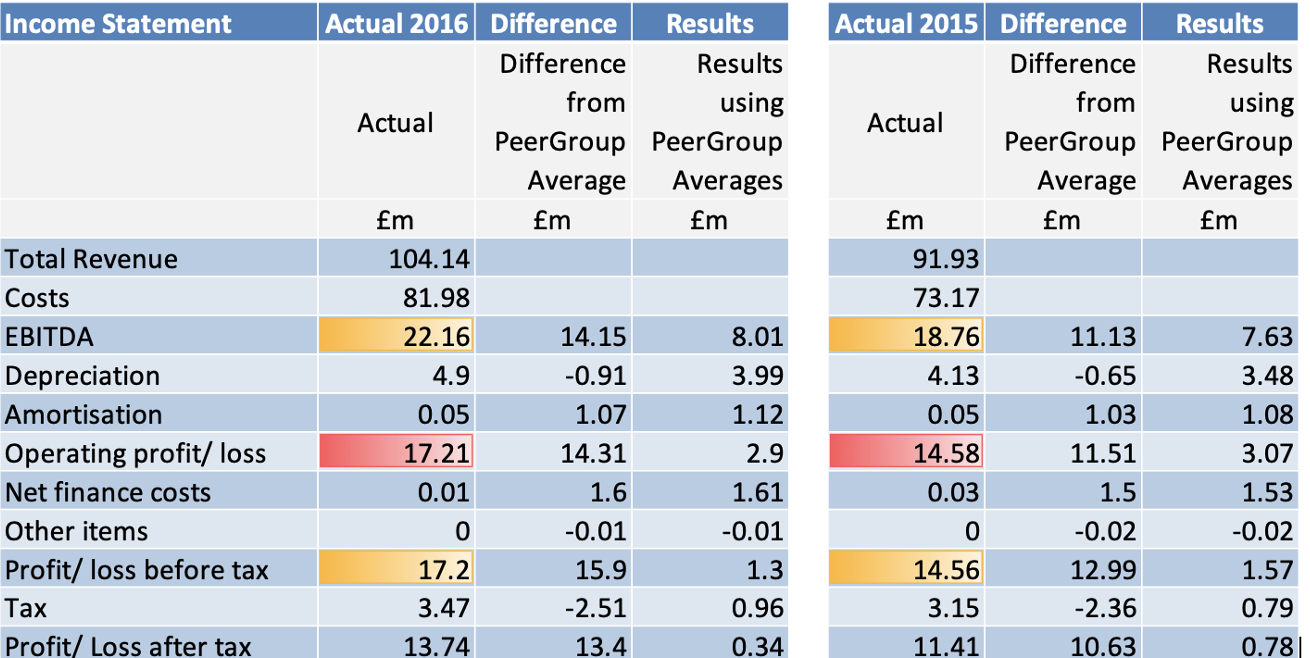

A benchmarking and risk-based approach would not only identify deviations but also quantify their significance. By comparing Patisserie Holdings' performance against its peers, it becomes evident that its EBITDA in 2016 was significantly above its peer group's average (see Illustration 2). Such findings could have guided auditors to focus their investigation on high-impact areas. Similarly, the system would have highlighted discrepancies on the Balance Sheet.

Illustration 2: Orange-shaded boxes show 1.0 to 1.5 standard deviations, pink-shaded boxes show standard deviations of over 1.5 (Source: Lavenham Solutions)

Looking ahead

The case of Patisserie Holdings showcases how a big data solution can play a pivotal role in preventing audit failures. A review of recent cases sanctioned by the Financial Reporting Council revealed that all of them could have been flagged using this method. Importantly, it only took me a few minutes to review the necessary information.

By harnessing the power of big-data-driven intelligence combined with a risk-based approach, auditors can identify early indicators of trouble, allocate resources efficiently, and restore confidence in the auditing process.

Olivier Beroud is co-founder of Lavenham Solutions a big-data analytics firm that offers auditors an effective tool to enhance productivity by quickly identifying red flags or areas of concerns. A longer version of this article can be found here: link. Olivier is also Visiting Professor at the LIBF. He was a member of the Financial Reporting Council’s Audit and Assurance Council from 2016 to 2020, and previously was Managing Director, Head of EMEA for Moody’s Investors Services until 2016.